This article first appeared in City & Country, The Edge Malaysia Weekly on February 26, 2024 – March 3, 2024

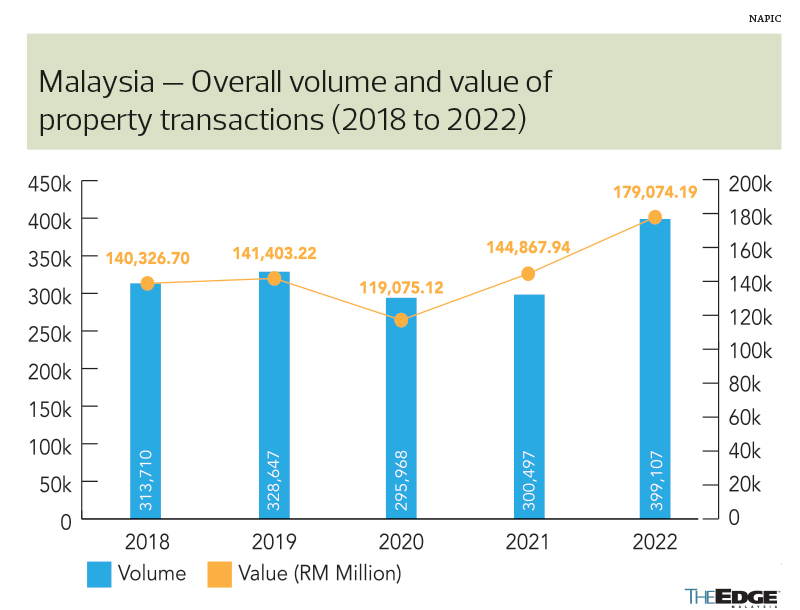

Malaysia’s property market is expected to maintain a more stable growth trajectory in 2024, following its recovery post-pandemic. In its report titled “HB Perspective 2024”, Henry Butcher Malaysia Sdn Bhd says that, for the first nine months of 2023, the overall volume of transactions was more or less maintained at the same level as 9M2022 while the value of transactions saw an increase of 8.8%.

“This indicates that the property market appears to have normalised and, although still growing positively, it no longer accelerates at the pace experienced when recovering from the low base of 2020/21. Nevertheless, the Malaysian property market will grow, but at a more gradual and sustainable pace,” the report explains.

The forecast positive economic growth could have a spillover effect on the property market this year, as the government has also expressed its confidence in achieving the growth forecast of between 4% and 5% for the year. The report attributes the expected growth in the country’s economy to “cautious yet improving” sentiment among property buyers and favourable government policies.

Although the country’s trade performance saw a decline in performance for the first 11 months of 2023, the report says economists are confident that the trade performance will show an improvement this year, owing to the anticipated resurgence of China’s economy and the implementation of the National Industrial Master Plan (NIMP) 2030.

Bank Negara Malaysia has not raised the overnight policy rate (OPR) and has maintained it at 3% since the last increase in May 2023. The report says, “Economists are projecting that Bank Negara Malaysia will keep the OPR at this level for the whole of 2024. This is positive for businesses and supportive of economic growth and will be beneficial for the property market.”

Steady residential market performance

The recovery in the residential property market, especially if it shows more signs of being sustainable, will inject optimism among developers, which may now launch more new projects as well as review and raise the prices of their new launches to cover the increase in construction costs due to the hike in the prices of building materials.

The report predicts that the focus of the residential property market in 2024 will continue to be on landed residential properties, high-rise apartments in the affordable price range in major towns and cities, smaller-sized units, niche high-end projects in good locations as well as projects with innovative concepts, designs and themes, which set them apart from the usual fare in the market.

In addition, the report says, areas that will be served by new major infrastructure projects will also be in demand, leading to more projects being undertaken by developers in these locations. Some of these infrastructure projects are the LRT system linking Penang Island and the mainland; the Rapid Transit System connecting Johor Bahru and Singapore; and the reinstatement of five previously cancelled LRT 3 stations in the Klang Valley — Tropicana, Raja Muda, Temasya, Bukit Raja and Bandar Botanic.

Meanwhile, Kuala Lumpur and Selangor are expected to lead this year in terms of volume and value of residential properties transacted as well as growth of house prices.

The report observes that the Johor market shows that buyers are more inclined towards 1- and 2-storey houses across both the primary and secondary markets. In Johor Bahru and Pontian, unsold stock is expected to be reduced in 2024.

Although the issue of overhang does not exist in Johor districts such as Kluang, Segamat and Mersing, the report says the take-up rate of properties there has been slow, which makes researchers think the market there might not be as active.

Nationwide, the report expects stamp duty exemption for residential transactions below RM500,000 for first-time home buyers until Dec 31, 2025, which was announced in Budget 2024, to aid in reducing the number of overhang properties.

Interestingly, the transaction records of Johor’s commercial-titled serviced apartments outperformed its market by a large margin in the first nine months of 2023 compared to the same period in the previous year. The highest number of transactions was recorded in 3Q2023, with 896 units valued at RM512 million.

The report says: “The momentum at which the market was moving looks promising to reduce Johor’s glaring overhang statistics as well as absorb some of the incoming supply of serviced apartments.”

Meanwhile, the stamp duty for foreign individuals and companies buying property in the country will be raised to 4% in 2024. The report says the hike in stamp duty is not helpful to the industry’s drive to attract more foreign investments in the real estate sector and runs counter to the government’s proposal to relax conditions under the Malaysia My Second Home (MM2H) programme.

Improved sentiment for office sector

According to the report, the office market benefited from improved business and consumer sentiment, following the country’s economic recovery after lockdowns and movement restrictions during the pandemic.

“The improved sentiment enabled businesses to recover and refocus on growth and this led to an increase in demand for new office spaces,” the report says.

“Some businesses have started to expand and new businesses have also sprouted up, leading to a rise in demand for office space. This pushed up the occupancy rates of office buildings in both Kuala Lumpur and Selangor in 2023.”

In line with the latest market trends and to accommodate the requirements of modern businesses, the report says, more new office buildings have been designed to be green-certified and equipped with better specifications.

The trend of businesses relocating outside the congested city centre has continued, especially with improved public transport, which has made these areas more accessible.

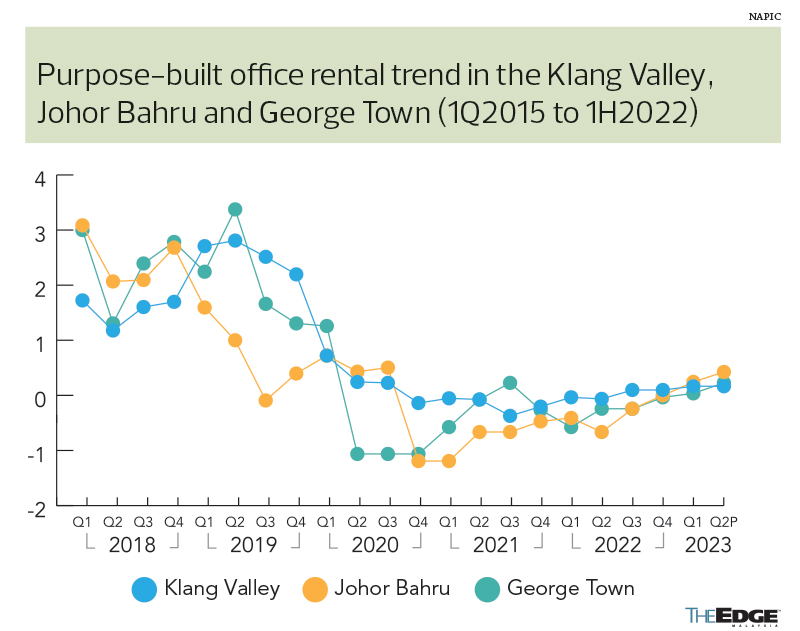

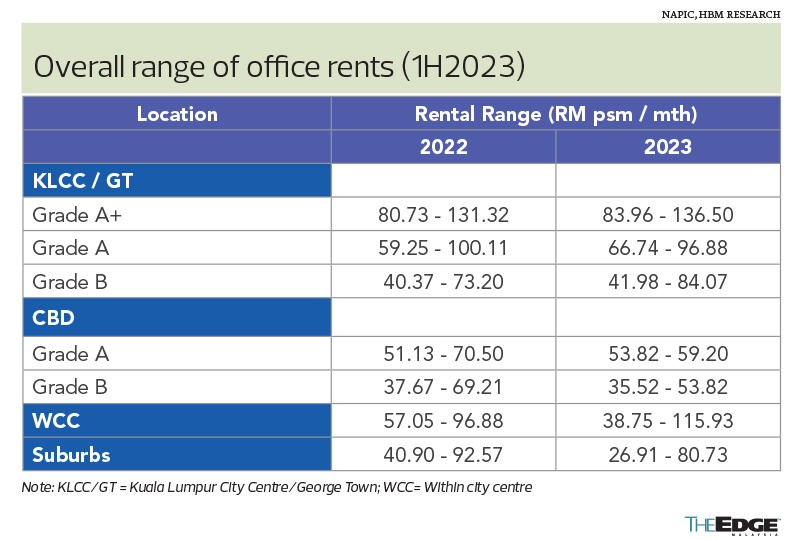

According to data from the National Property Information Centre (Napic) for the first two quarters of 2023, the rental index for purpose-built offices (PBOs) for the Klang Valley registered a marginal increase of 0.1%. The report says this is due to an increase in the take-up of office space, which led to an improvement in occupancy rates.

In terms of the overall range of office rentals, Grade A+ space in Kuala Lumpur City Centre and George Town, Penang garnered the highest rents from RM83.96 to RM136.50 psm per month. The report says this shows that higher-grade offices are currently the most sought after in the market.

The completion and availability of high-quality office space in new integrated commercial developments such as Tun Razak Exchange, KL Eco City and Pavilion Damansara Heights have attracted businesses to relocate to these new business hubs.

“Nevertheless, a significant amount of office space will come onto the market over the next few years, and this is expected to put pressure on occupancy rates and could lead to a softening of rental rates as landlords compete to fill up their buildings,” the report says.

“Newer buildings with better specifications and more facilities as well as higher compliance with ESG (environmental, social and governance) standards will generally be in a better position to attract tenants than older buildings that have not been upgraded. In the future, more of the older buildings will be upgraded, taken over or repurposed to other uses like hotels, serviced apartments or senior living accommodations.”

In Penang, PBOs are expected to see a modest increase this year in transaction volumes and values, higher rental rates and a potential for improved occupancy rates — reflecting a generally optimistic outlook for the subsector. The report contributes this to factors such as the state’s economic stability and evolving work patterns such as hybrid and flexible work arrangements.

Retail sector to grow despite challenges

Based on the report, the business confidence survey conducted by the Malaysian Institute of Economic Research (MIER) for 3Q2023 saw business confidence hit a low of 79.7 points, which is a year-on-year decrease from 99.8 points. The Consumer Sentiment Index shows a similar drop to 78.9 points, from 86 points y-o-y.

“This may mean businesses as well as consumers may adopt a more cautious stance and may want to defer spending on big-ticket items like property as well as acquiring new premises for business expansion,” the report says.

It explains that the prospects of the Klang Valley shopping centre market in 2024 remain highly dependent on the performance of the Malaysian economy and how well the government navigates challenges such as international conflicts and economic slowdowns experienced by its major trading partners as well as the purchasing power of local consumers.

The retail sector in the Klang Valley may, however, face oversupply challenges this year, the report says. “[Because of that], existing shopping centres will continue to struggle to secure new tenants and achieve high occupancy rates. Retail landlords of shopping centres will need to offer lower rental rates, longer renovation periods and base rent with turnover rent to attract quality tenants.”

New shopping centres in the Klang Valley that opened in 2023 include Pavilion Damansara Heights Mall at Damansara Heights, with a net floor area (NFA) of 533,361 sq ft; The Exchange TRX at Jalan Tun Razak, with an NFA of 1.3 million sq ft; and KSL Esplanade Mall in Klang, with an NFA of 700,000 sq ft.

In Penang, the retail sector is expected to improve this year, encouraged by factors such as increased tourism and economic growth. The report also says that amid the growing wave of budget retail developments in Penang, other innovative projects such as Iconic Point in Simpang Ampat have also pushed up property prices and rents in their locality.

Other prime malls in Penang have also enjoyed increased footfall and improved occupancy rates. “Judging from [these points], Penang’s retail sector appears to be recovering in 2023, boosted by a growing tourism industry post-pandemic. This has led to the mushrooming of tourism-related businesses such as restaurants, cafés and budget hotels in traditional shophouses, more so in the George Town city area,” the report says.

Like the rest of the country, Sarawak also saw an increase in supply of budget-conscious stores. At the same time, the report says, the state saw the same trend of the opening of more F&B outlets, smaller anchor tenants and specialist branded stores. As such, the retail sector in Sarawak is expected to continue to perform well in 2024.

Industrial remains most vibrant

The report says the implementation of the NIMP 2030 is expected to provide a boost to the country’s industrial sector, which will in turn lead to an increased demand for industrial space.

In Selangor, the state government has announced plans to develop a Selangor International Aero Park adjacent to the Kuala Lumpur International Airport in Sepang and has begun talks with stakeholders.

“Selangor recorded a 75% increase in the value of the total capital investments approved for manufacturing projects in the state for the first nine months of 2023 compared to the corresponding period the year before and this is expected to boost demand for industrial land and buildings in the state,” the report says.

In 2024, prices of industrial development land in Penang are expected to rise, given the strong demand and limited industrial land supply.

Construction of the newly announced Silicon Island has begun and will take 25 years to be completed. The Penang government aims to reclaim 400 acres annually for the project, with a targeted rollout of the first factory by 2026.

Henry Butcher Malaysia says five acres have already been reclaimed since work commenced in October 2023, with dredging work intensifying this year. The developer aims to complete the land component in eight to 10 years or as early as 2032. Developments at the project will include a Green Tech Park, a global business services and software hub, and the development of commercial and housing real estate.

The report says: “Despite the lofty plans, things could still go wrong if, for example, [the Penang government] neglects rural and semi-urban areas, and [this could risk] imbalanced growth throughout the state. Another potential risk is the absence of proven strategies to revive the commercial and retail sectors, which are crucial for post-pandemic recovery. This could curtail any possibility of a resurgence and impact the property market’s interconnected growth.

“While urbanisation and industrialisation may take precedence, [a lack of] sustainable practices could yet stir up long-term environmental repercussions and derail Penang from aligning with global climate trends.”

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.